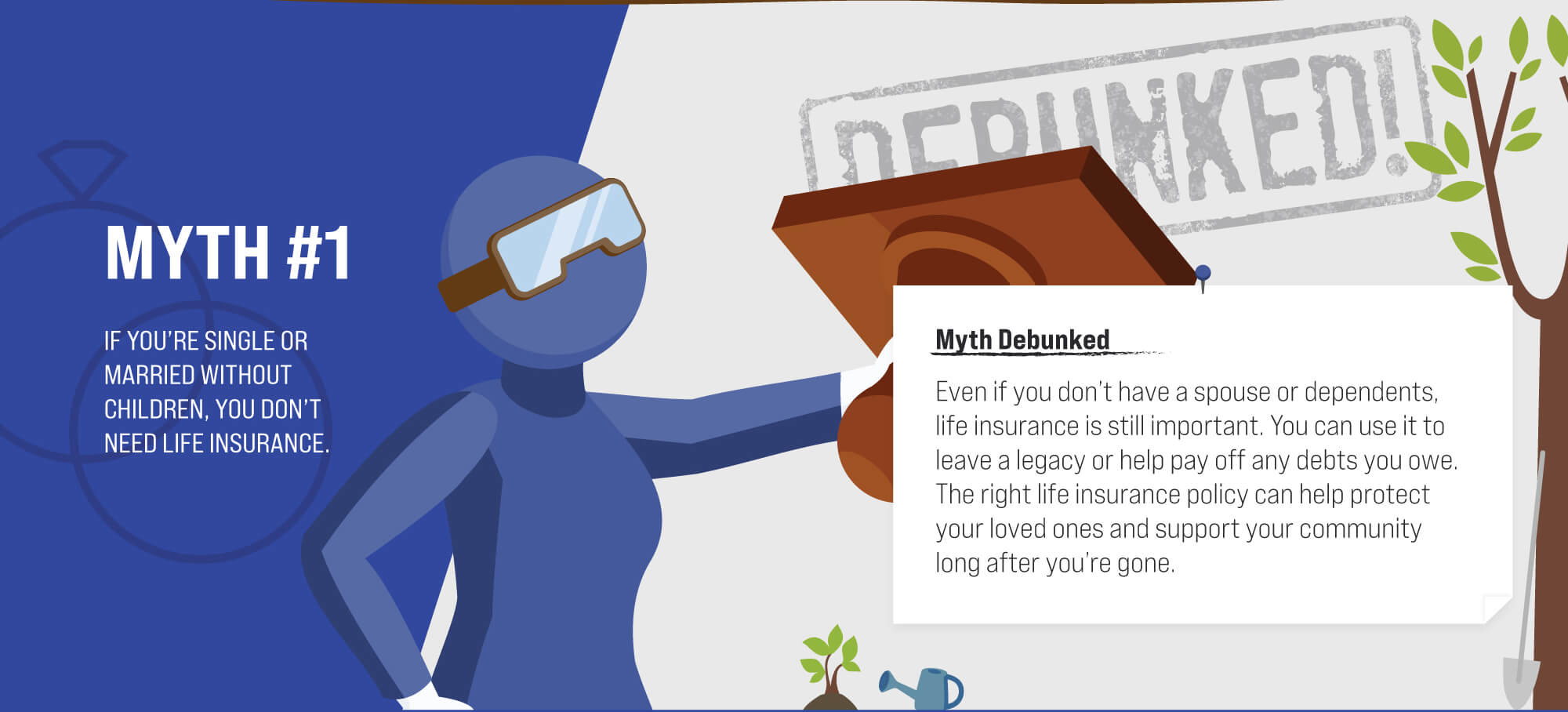

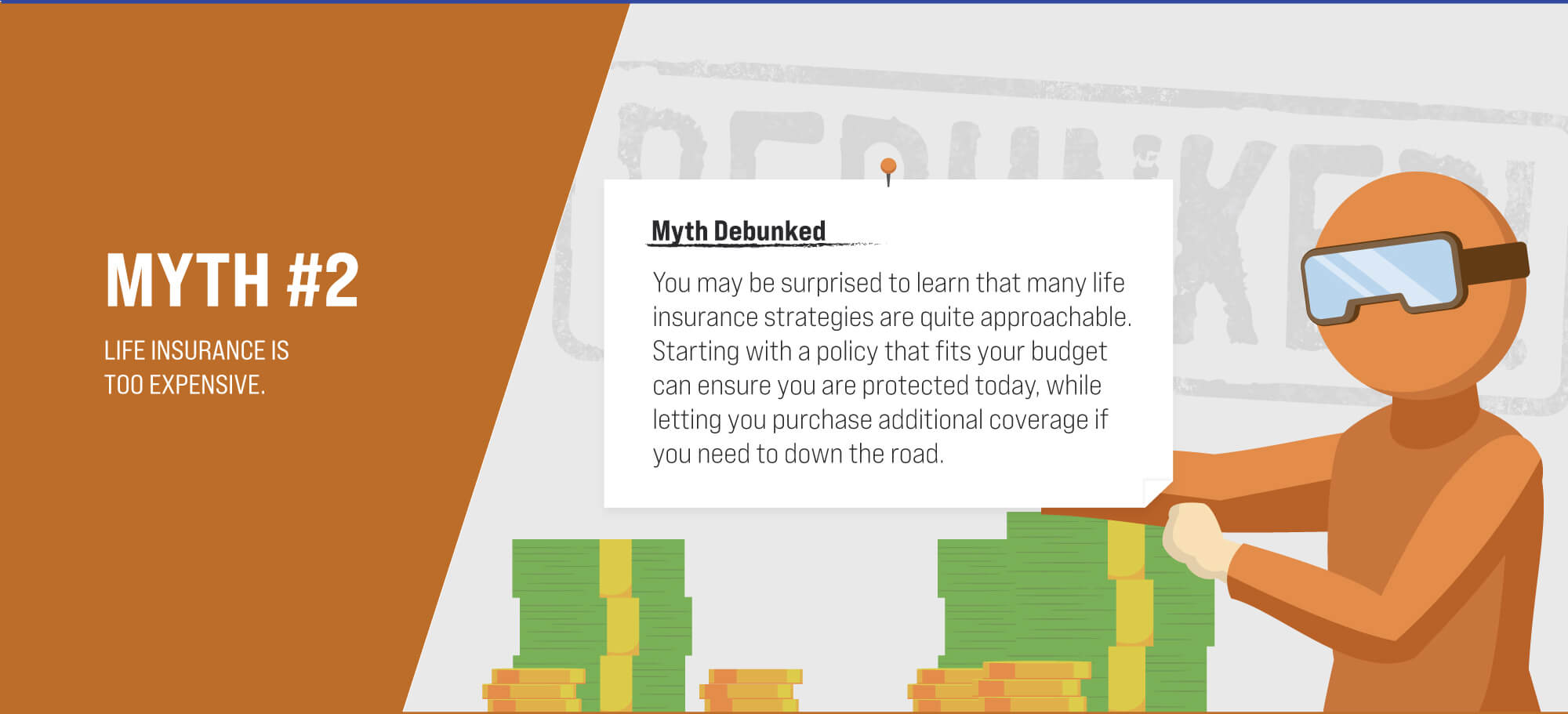

Life Insurance Myths: Debunked

Term insurance is the simplest form of life insurance. Here's how it works.

Solve a mystery while learning how important your credit report is with this story-driven interactive.

Use this calculator to better see the potential impact of compound interest on an asset.